News

When the Bridgetown Initiative for the Reform of the International Financial Architecture (IFA) was released in autumn 2022, it caused quite a stir, especially in the climate finance community. Promoted by Mia Mottley, the strong-willed prime minister of Barbados, the initiative influenced the UN climate summit in Sharm-el-Sheikh and inspired the Summit for a New Global Financing Pact organised by French president Macron in Paris in June 2023. The second version, Bridgetown 2.0, was released in time for the UN climate summit in Bonn in June 2023, and looked like a merger with the SDG Stimulus Package being promoting by the UN through its Secretary-General, António Guterres. Just in time for the 4th International Conference on Small Island Developing States in Antigua and Barbuda, Barbados has rolled out an updated version, Bridgetown 3.0. So what´s new?

{kind=link}

All three versions share the same goal: to mobilise vast amounts of additional finance to fill the gaping holes in both climate and overall development finance. Bridgetown 1.0 was clearly structured around liquidity measures, mostly related to reformed International Monetary Fund (IMF) facilities and instruments, and development finance measures to be taken by the Multilateral Development Banks (MDBs). The third pillar in Bridgetown 1.0 was a multilateral instrument financed by Special Drawing Rights (SDRs), supposed to mobilize private investments for climate change mitigation. Bridgetown 2.0 was somewhat more comprehensive and disaggregated, adding, for example, some vague policy recommendations on tax and trade, debt relief, and non-monetary aspects of IFA-reform, such as access criteria to concessional loans or governance reform.

I have commented extensively on Bridgetown 1.0 in an earlier blog, and on Bridgetown 2.0 at a side-event at the Bonn Climate Change Conference in 2023. The matrix here compares all three versions of the Bridgetown Initiative using the original texts, structured along the themes as they appear in the latest version. The rest of this blog is to check what’s new in Bridgetown 3.0 and, perhaps no less interestingly, what’s been lost.

Innovations in Bridgetown 3.0 vs 2.0

At least four new areas of policy reform are entirely new in the new version:

- Credit Rating Agencies: “Credit Rating Agencies must play their part and overhaul end the current systemic rating biases against small, poor and vulnerable countries, their methodologies to and specifically to capture longer term financial health.”

- Carbon Pricing: “All governments must establish a carbon price taking into account the Paris principles and their level of development. Governments should further support the development of a Global Carbon Pricing Framework that is just and equitable and task the International Institutions to deliver on this.”

- SDR allocation: “The IMF and its shareholders must achieve agreement on a new $500bn issuance of SDRs.” (Bridgetown 1.0 had called for additional SDRs, but version 2.0 did not.)

- Philanthropic GPG financing: “Philanthropic organizations must agree to a Global Compact through which a defined portion of their financing would go to GPGs.”

None of these point are actually entirely new, or new in the sense that Bridgetown 3.0 introduces them into discourse and policy-making. The problematic bias of credit rating agencies, which boosts the costs of private finance for developing countries, has been a feature of all major policy debates since the COVID-19 crisis. This included in the negotiations leading up to the UN´s Summit of the Future in September, where developing countries in particular pushed for a new SDR allocation. Discussions on the wider adoption of carbon pricing also took place at the G20 and at the Paris Summit, where the role of philanthropy in financing global public goods (GPGs) was also a topic. By adding these items, Bridgetown 3.0 is not innovating, but simply tracking the discourse that is taking place elsewhere.

Modifications in Bridgetown 3.0 vs 2.0

Most policy recommendations in continued policy areas received slight modifications. Some of the more substantial ones are:

- Mobilisation targets: Version 2.0 has set a mobilisation target of 1.5 trillion per year in private investments for a green and just transformation. This has been reduced to USD 500bn per year, for mitigation and adaptation. Whereas Bridgetown 1.0 called for an additional USD 1 trillion in MDB lending, version 3.0 calls for an extra USD 300 billion per year.

- Specific taxes: While version 2.0 had mentioned taxes for the first time, the third version gets much more specific, calling on countries to “establish a levy on fossil fuel company windfall profits, financial transactions, and emissions on shipping and aviation to help finance GPGs, and define a governance framework for their use.”

- SDR rechannelling: The Inter-American Development Bank (IADB) is also mentioned as a potential actor to work with SDRs, alongside the IMF and the AfDB.

The reduction in mobilisation target is notable. This sounds pragmatic as even the reduced targets will be difficult to achieve, but there are no evidence that financing gaps and financing needs are shrinking in the real world. The addition of new actors to the SDR channels is due to the fact that the IMF Executive Board recently approved the rechannelling of SDRs through the MDBs. While the AfDB was first to establish adequate financing instruments, the appetite of other MDBs, notably the IADBs, has been whetted.

Perhaps the most important change here is the new language on tax. Taxes have become a big issue of late, partly because the UN General Assembly´s Ad Hoc Committee on International Tax Cooperation started work earlier this year, and an informal new International Tax Task Force was set up, co-chaired by France, Kenya and Barbados. Unsurprisingly, the list of taxes selected for Bridgetown 3.0 mirrors that of the Task Force. Omitted are some of the tax types with the greatest revenue potential, such as reformed corporate taxes or wealth taxes (billionaire taxes) which tend to be controversial in low-tax jurisdictions, despite the fact that these tax types are high on the agenda of the UN Committee and the G20.

Deleted from Bridgetown 2.0:

Some highly relevant aspects are no longer included in the new version, and in some cases one wonders why:

- MDB capital increase: “Put an additional $100 billion of paid-in capital contributions into MDBs.”

- “Better” banks: “Streamline and harmonize loan procedures across MDBs and IFIs, increase front-line support to countries accessing loans, and finance country-led national resilient development plans and multi-country programs that protect the global commons.”

- Supply Chains: “Work with governments to ensure supply chains become resilient, benefit raw materials producing nations and protect the vulnerable.”

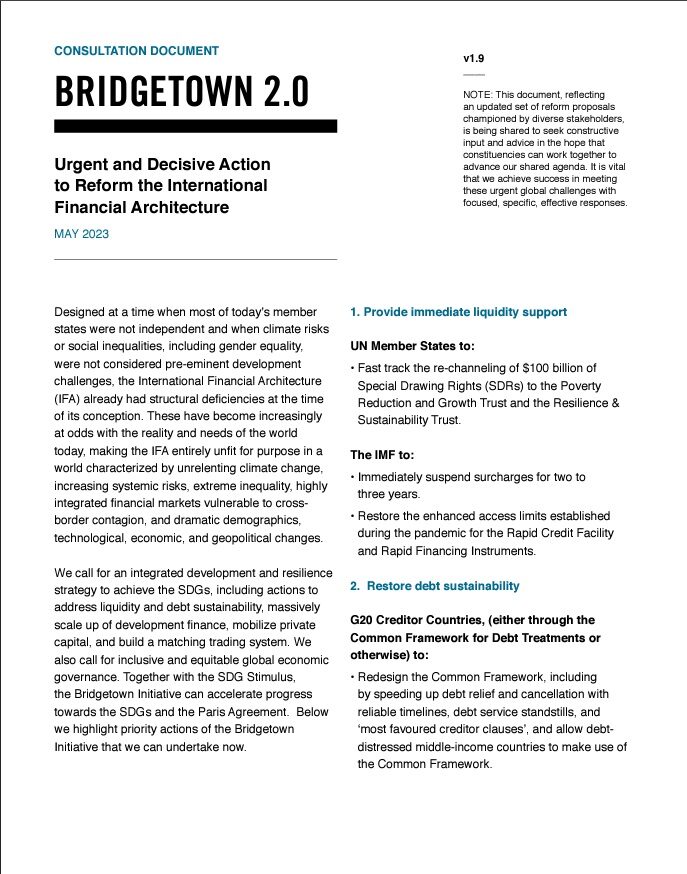

- Debt relief: “Redesign the Common Framework, including by speeding up debt relief and cancellation with reliable timelines, debt service standstills, and ‘most favoured creditor clauses’, and allow debt-distressed middle-income countries to make use of the Common Framework (…). Encourage the restructuring of unsustainable private debt through IMF programs that are consistent across countries and have more locally driven fiscal sustainability plans.”

When it comes to new money for MDBs, the focus has shifted from the MDB capital increases to IDA replenishment. IDA replenishment is indeed on the agenda this, while capital increases face some political hurdles and have a longer way to go. When it comes to demands on better banks, it is notable that harmonization and streamlining have been removed, as there is considerable pressure on MDBs to ´work better as a system´. Talking about supply chains would certainly complicate things these days, so why go there when you want to talk mainly about finance.

Most strikingly, however, all measures related to debt reduction, debt cancellation and reform of the international debt architecture have been removed from the Bridgetown Initiative as it stands now. The only exception is a call for creditors to adopt natural disaster clauses – a liquidity instrument that temporarily suspends, but that does not reduce debt service obligations. This move is all the more striking given that Bridgetown 1.0 already had acknowledged that many countries lack the absorptive capacity for additional lending, and the situation worsened over the past two years as interest rates have soared.

Moreover, one of the main criticisms over the past two years has been that the Bridgetown Initiative is too “debt-heavy”, recommending too many instruments that create debt, while neglecting grant and tax instruments that do not. This was probably the reason why the tax language was first added in Bridgetown 2.0, and finally strengthened in Bridgetown 3.0. While better tax language is certainly welcome, it makes no sense to delete all debt-reducing instruments from the policy package makes no sense. It helps Bridgetown-apologists out of the dilemma that adopting the policy package might push many countries over the brink of debt crises, but turning a blind eye to the debt problem is turning a blind eye to the central challenge of development finance today.

Next step implementation

Having said that, Bridgetown 3.0 carried forward many good reform recommendations from previous versions, which were not mentioned in this blog but are listed here for comparison. Implementation, of course, remains the key challenge. The chapeau of the latest version already mentions that too little has happened since the first version came out, and the conclusion sets the end of 2025 as a hard deadline for implementing the package. The 4th International Conference on Small Island Developing States did not bring much progress – the main innovation was to consider setting up a “dedicated small island developing States debt sustainability support service". Key milestones in the political calendar are the Summit of the Future in September 2024, the UN climate change conference in Baku in November, and finally the Fourth International Conference on Financing for Development in Spain in June 2025.